If you are forcibly retrenched or take voluntary retrenchment, your company will typically pay you a severance benefit, a retrenchment benefit, the monetary value of your notice period (if you don’t work out your notice period) and the monetary value of any outstanding leave you may have. It is important to know how these different payouts are taxed, as they are taxed at different rates.

The latter amounts (the monetary values of your notice period and outstanding leave) are taxed according to your marginal tax rate, as they form part of your normal remuneration and do not form part of the severance pay.

It is important to note that there is a difference between a severance benefit and a retrenchment benefit.

• A severance benefit is the amount of money you receive from your employer as a result of the retrenchment process. In terms of the Basic Conditions of Employment, it is equivalent to at least one week’s remuneration for every full year worked at your current employer. This severance benefit cash lump sum can also be paid to someone who is being offered early retirement (they must be 55 years or older), or whose employment is terminated due to permanent incapacity (such as in the case of terminal illness).

• A retrenchment benefit refers to your retirement benefits in your company’s pension or provident fund that you will have to decide what to do with. It is most commonly the same benefit that you would receive from the fund if you resigned. You will generally have the following options regarding your retrenchment benefit: take the benefit as a cash lump sum, transfer the benefit to a preservation fund, or a combination of the two.

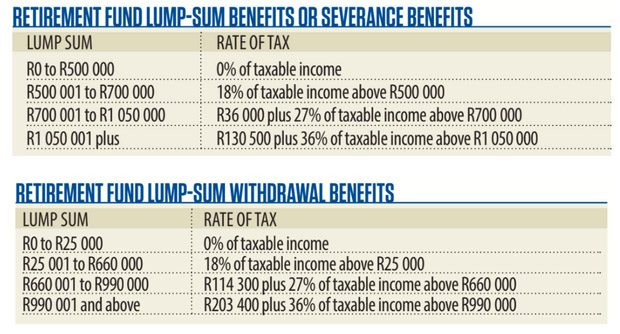

For both severance benefit payments and retrenchment cash lump sums, the taxable portion of the lump sum is taxed according to the “Retirement fund lump-sum benefits or severance benefits” tax table, taking into account prior retirement fund lump sums received. These rates are far lower than those in the “Retirement fund lump-sum withdrawal benefits” tax table, which applies if you resign from your job and take your retirement savings as a lump sum.

If your exit is processed as a resignation, your retirement fund cash lump sum will be taxed on the much more stringent withdrawal tax table. Whether it is voluntary retrenchment (where you opt in to the initial rounds of the retrenchment process) or involuntary retrenchment (when there is no option), you should ensure that your exit is processed as retrenchment and not a resignation.

While you will be paid your severance benefit as a cash lump sum, it is up to you to decide whether you want to fully or partially take your retrenchment benefit as a lump sum or preserve it in a preservation fund.

As the severance benefit and retrenchment cash lump sum benefits are taxed according to the retirement tax table, the first R500 000 of your taxable retirement fund lump sums is taxed at 0%. However, the tax-free R500 000 is a once-off concession over your lifetime. The retirement tax table is only applied to lump sums taken when you are retrenched, when you retire, or on your death. This means that at a new company in the future, if you are retrenched again or you retire, the concession will not apply if you already received a prior severance benefit lump sum of R500 000 or more during the first retrenchment (after 1 March 2011). If your severance benefit lump sum was, say R200 000, then it means that you have a tax-free concession on a lump-sum benefit of up to R300 000 on a subsequent retrenchment or at retirement.

Article: IOL