MONEY BASICS WITH MARTIN HESSE

There is a common misunderstanding about income tax, which goes something like this: you are due for a raise but are worried that the raise (which may be relatively small) will push you into a higher tax bracket, and this will cancel out the raise because of the higher percentage of your earnings going to the taxman. In fact, you may be worried that you might get out less after tax than you were getting before.

But that is not how the brackets in the South African Revenue Service’s income tax tables work. A jump to the next bracket will never result in a reduction in income going into your pocket.

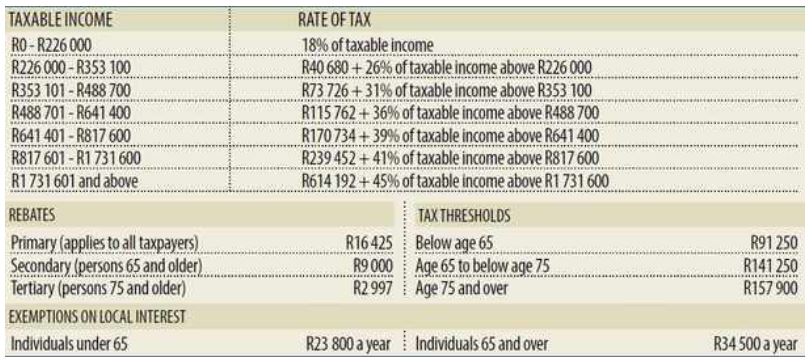

As you can see from the tax table (which applies to the 2022/23 tax year), the brackets are 18%, 26%, 31%, 36%, 39%, 41% and 45%. If, say, you fall into the 36% bracket, you are not paying 36% on all your income; you are paying 36% only on anything you receive above R488 700.

You are taxed in steps that progressively take a larger portion of your income. Picture the brackets as rungs on a ladder: you are taxed less on income that falls into the lower rungs than income that falls into the higher rungs. Hence the tax brackets are known as marginal brackets.

For example, say that, after deductions, your taxable income for the year is R500 000. You pay tax of:

- 18% on the first R226 000 = R40 680

- 26% on the next R127 100 (which is R353 100 – R226 000) = R33 046

- 31% on the next R135 600 (which is R488 700 – R353 100) = R42 036

- 36% on the next R11 300 (which is R500 00 – R488 700) = R4 068

- Total tax before rebate: R119 830.

- Total tax after the primary rebate of R16 425: R103 405.

- Percentage of R500 000 going to SARS: 20.68%

The actual percentage of your income going to SARS is known as your average tax rate. The rates indicated in the table are known as the marginal rates.

So, to recap, on a taxable income of R500 000, your marginal rate is 36% (meaning that you are in the bracket whereby any additional income you accrue is taxed at 36%), whereas your actual, or average, rate is 20.68%.

What if your income had been R480 000 – in other words, you fell within the 31% marginal bracket?

We don’t have to go through all the sums again, because SARS has worked them out for us in the table. According to the table, your tax is R73 726 plus 31% of the amount above R353 100. The amount above R353 100 is R480 000 – R353 100 = R126 900. Therefore your tax is R73 726 plus 31% of R126 900 = R73 726 + R39 339 = R113 065. If you subtract the rebate of R16 425, your final tax bill is R96 640. This translates into an average tax rate of 20.13%.

So let’s revisit that original concern. Your income is R480 000 and you are worried that a small raise of R20 000 will push you from the 31% marginal bracket into the 36% marginal bracket, resulting in less money in your pocket.

On R480 000 your tax after the rebate is R96 640, translating into an average rate of 20.13%.

On R500 000 your tax after the rebate is R103 405, translating into an average rate of 20.68%.

So, in this example, for an extra R20 000 income, you will pay an extra R6 765 to SARS, but R13 235 will go into your pocket.

Deductions, rebates and tax credits

Tax terms can be confusing – among others you get deductions, rebates, and credits:

Deductions: these are qualifying expenses and retirement fund contributions that you can deduct from your overall (gross) income. Once you have subtracted these amounts, you are left with your taxable income for the year. It is on this taxable income that the SARS tax tables apply. In other words, deductions are applied before the tax calculation.

Rebates: these are amounts SARS gives back to you on the tax you owe. In other words, rebates are applied after the tax calculation.

Tax credits: these apply to medical expenses and to contributions to a medical scheme. They apply like rebates – in other words, the credit amount is given back to you after the tax calculation.

Article: IOL